Scan QR code or get instant email to install app

Question:

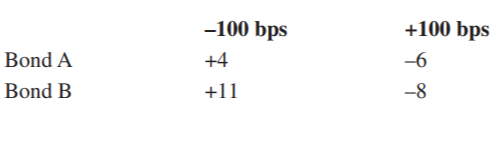

The following information relates to two callable bonds of the same issuer that are currently callable.

Both the bonds have the same maturity and the yield curve for the issuer is flat. Which of the bonds is most likely the higher coupon bond?

Estimated Percentage Change in Price if Interest Rates Change by:

A

Bond A

explanation

• At current yields, Bond A exhibits negative duration, as the percentage price decrease from an increase in interest rates (–6%) is greater than the percentage price increase from a decrease in interest rates (4%). Given the current level of interest rates, Bond A must be the higher coupon bond as it is undergoing “price compression.” Bond A is likely to be called, as its coupon rate is greater than market yields.

• Bond B exhibits positive convexity. It is not in danger of being called so its coupon rate must be lower than current market interest rates.

Take more free practice tests for other PASSEMALL topics with our cfa practice questions now!

Related Information

Comments