Scan QR code or get instant email to install app

Question:

Based on these spreads, it is most likely that:

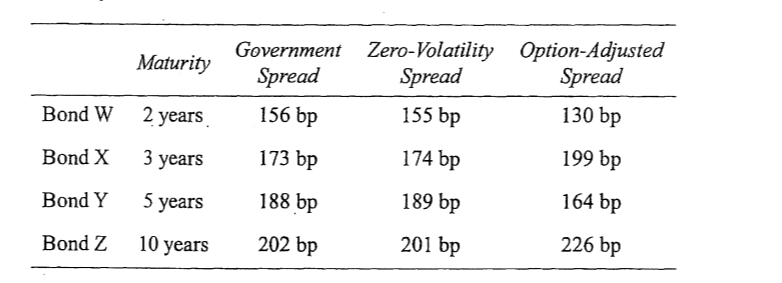

Four non-convertible bonds have the indicated yield spreads to Treasury securities:

A

Bond W is callable, and Bond Z is putable.

explanation

Bonds W and Y are most likely callable, and Bonds X and Z are most likely putable. If the option-adjusted spread is less than the zero-volatility spread, the embedded option has a negative value to the bondholder (e.g., a call option), and if the option-adjusted spread is greater than the zero-volatility spread, the embedded option has a positive value to the bondholder (e.g., a put option). Zero-volatility spreads adjust for the fact that nominal spreads (between the yields to maturity of two bonds) are theoretically correct only when the spot yield curve is flat. All of these bonds’ zero-volatility spreads are nearly identical to their government spreads, which suggests the spot yield curve is approximately flat.

Take more free practice tests for other PASSEMALL topics with our cfa mock exam now!

Related Information

Comments